Old ILIT New Solutions

An “ILIT” is an Irrevocable Life Insurance Trust. One of the purposes of an ILIT is to prevent life insurance benefits from being taxed. (Yes, although generally income tax free, life insurance can be subject to an estate tax.) This only works if the ILIT is structured properly and used correctly. Variations of an ILIT can also be used for many other purposes such as providing for blended family situations, asset protection, business succession, or Special Needs planning. If there is a need for an ILIT, there is also a need for Dynasty Provisions. In Old ILIT New Solutions, we address the problem of how to update, upgrade, or modify a Trust that is irrevocable.

Old ILIT

An ILIT can become obsolete. This happens when its purpose no longer applies or circumstances change. For example, with new higher estate tax exclusions, many life insurance policies that would have been taxed in the past, no longer have that problem. Changes in the family, health, finances, the life insurance policies and other factors may also render an ILIT out-of-date.

New Solutions

The word “Irrevocable” frightens many people, including too many attorneys and life insurance professionals who should know better. “Irrevocable” may mean not revocable or amendable, but it does not mean unchangeable. And it does not mean once set up you must live with an ILIT forever no matter how the world around it may change. There are many ways to “update” an Old ILIT. Here are just a few of the most common approaches.

- Administer it According to Its Terms. A well crafted ILIT will have built in ways to make updates. For example, under the terms of the Trust instrument, it is often possible to change Trustees, modify allocations among beneficiaries (powers of appointment), change domiciles, and make other administrative adjustments.

- Family Settlement Agreement. Some Trust instruments, and a number of local state statutes, permit a Trust to be modified by agreement of the parties. All concerned must have notice, and sign on to whatever the changes may be.

- Go To Court. If the parties cannot agree, they can always petition the Court to approve or even order adjustments to the Trust. Court’s may often take actions that the parties may not have the power to do. This is my least favored of all the options, but it is sometimes a necessary and appropriate measure, particularly when there is not a consensus.

- Protector Action. A better written ILIT will have what is called a Trust Protector. The Trust Protector may have a number of powers, including in some instances the ability to make certain changes to the Trust.

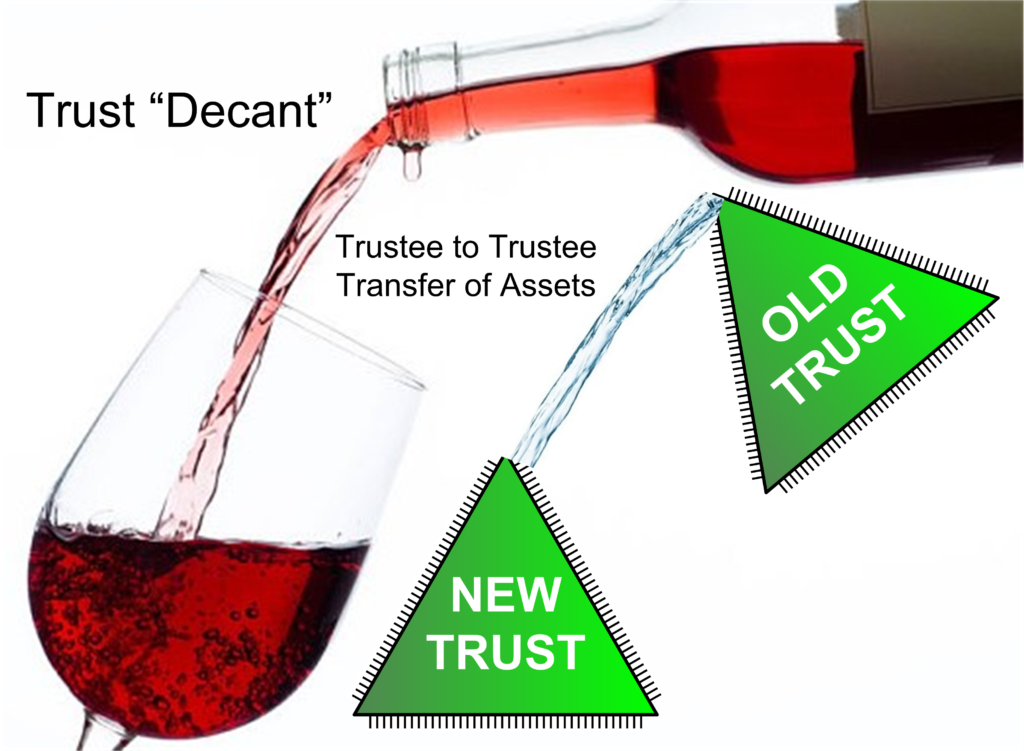

- Decant. “Decanting” a Trust is a new name for an old practice used for many decades by knowledgeable attorneys. Its recent recognition by the Uniform Trust code has made it more popular with some attorneys who previously believed it was not possible. Decanting a wine refers to pouring it from one container to another for the purpose of improving its taste or other qualities. In a similar fashion, “decanting” a Trust involves pouring the assets of one Trust into a new Trust. This involves forming a new Trust then transferring assets from one Trustee to another. The power to do this may arise by the terms of the Trust itself, or in some instances by local statute.

- Unwind. Although it is “irrevocable” an ILIT can, without question, be shut down. The assets (life insurance policies) can, of course, be distributed to the beneficiaries. That is typically the children of the insured and/or the Grantors. However, this may not always be the best. Sometimes for simplification purposes or access to cash value or death benefits, the insured or the Grantors of the ILIT want to recover ownership of the life insurance. I have heard attorneys take the hard line approach that an ILIT simply cannot distribute the life insurance policy to the insured. This is only partially correct. The practical reality is that an ILIT cannot distribute a life insurance polity to the insured WITHOUT TAX CONSEQUENCES. It is the penalty, or lack thereof, that makes all the difference. In many instances, based on the value of the policies and the size of the taxable estate of the insured, THE TAX CONSEQUENCES MAY BE ZERO. In such instances, if there is no tax penalty, there may be no problem. Even if the policies take a circuitous route (distribute to the children, who then gift it back to their parents), one way or another it is often possible to cause the life insurance to be owned by the desired party without adverse consequences.

Old ILIT New Solutions — The Decant

Of course, getting qualified legal advice before implementing any of these solutions is crucial. Applying new solutions to an old ILIT often requires a team — the policy owner, the insured, the insurance professional, the family CPA, and legal counsel. Don’t let anyone tell you an ILIT cannot be changed or updated. But don’t try it alone.

Can an Irrevocable Trust be Changed?

The answer is, of course, yes. Knowing how makes all the difference. Can an Irrevocable Trust be “revoked”? Irrevocable means no revoking, but it does not mean no changing. Can an Irrevocable Trust be amended or changed without revoking it? Of course. Irrevocable Trusts change all the time. Assets change. Trustees change. Beneficiaries change. Change is inevitable. Who makes the change, and how the change happens determines whether or not the purpose of the Irrevocable Trust is preserved or frustrated.

Get Help

With the adoption of the Uniform Trust Code, the Trust “Decant” was given a name and became better known and more acceptable in the legal community. It is not new. We have been using this tool long before it had a name or became popular. There are best practices for Old ILIT New Solutions. We will review your existing Trust on a complimentary basis. Let us know. If you have questions or would like to explore your options, we can help @4803248000.